Top 5 Web3 Applications Revolutionizing Industries in 2026

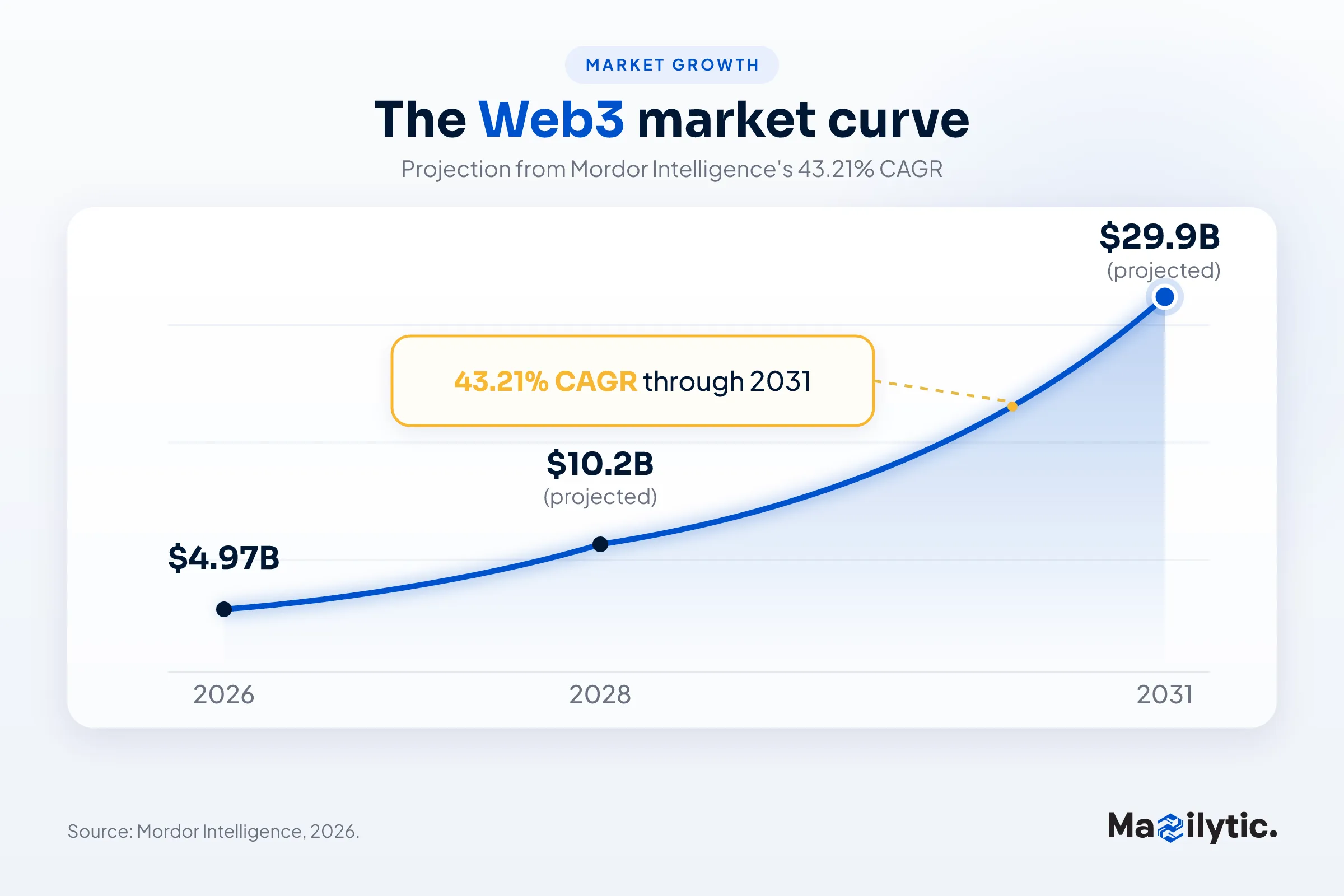

Web3 is no longer a pitch deck concept; it's more like an operating infrastructure. After the speculative excess of 2021 to 2022 and the "utility or bust" correction of 2024 to 2025, the applications built on decentralized rails have entered a more disciplined, revenue‑driven phase in 2026. Analysts at Mordor Intelligence estimate the global Web3 market will reach roughly $4.97 billion in 2026, expanding at a compound annual growth rate of 43.21% through 2031 as enterprise adoption, regulatory clarity, and mature developer tooling replace hype‑driven cycles.

Other estimates place the figure higher: Research and Markets puts the 2026 Web3 market at $12.61 billion, growing to $51.54 billion by 2030, but nearly every forecaster agrees on the direction: steep, sustained growth built on functional applications rather than speculative ones.

This guide walks through the core technologies behind Web3, the five categories of Web3 applications reshaping industries in 2026, and the trends worth watching as the sector matures.

A Quick Refresher: What Is Web3?

Web3 describes an internet architecture built around decentralization, verifiable ownership, and reduced reliance on centralized intermediaries. Instead of a handful of platforms controlling identity, data, and value exchange, Web3 applications, often called decentralized applications, or dApps, run on blockchain networks where rules are enforced by code (smart contracts) rather than by a company's internal database.

Three technologies anchor this shift:

- Blockchain infrastructure: including Layer‑1 networks such as Ethereum and Solana, and Layer‑2 scaling solutions that reduce fees and increase transaction throughput.

- Smart contracts: self‑executing agreements that automate lending, trading, governance, and ownership transfer without a middleman.

- Tokenization: the process of representing an asset, financial, digital, or physical, as a blockchain‑native token that can be transferred, fractionalized, or programmed.

By 2026, a fourth layer has become just as important: regulation. The U.S. GENIUS Act (2025) created the first federal framework for stablecoins, requiring full reserve backing and monthly disclosures, while the Clarity Act, moving through Congress in 2026, aims to formally distinguish digital commodities from securities. In the EU, MiCA and DAC8 have raised compliance costs but given institutions the legal certainty to deploy real capital on‑chain. This regulatory scaffolding is a large part of why Web3 applications look different and more durable in 2026 than they did during the previous cycle.

Why Web3 Applications Matter in 2026

The core promise of Web3 development hasn't changed: shifting control of data, assets, and governance away from centralized platforms and toward users. What has changed is who's building on it. Institutions such as BlackRock, JPMorgan, and Fidelity have moved from sandbox pilots to production deployments of tokenized funds and settlement systems, and enterprises are increasingly hiring a Web3 development company to build compliant, audited applications rather than experimental ones. Below are the five categories of Web3 applications doing the most to reshape industries this year.

1. Decentralized Finance (DeFi)

DeFi remains the largest and most closely watched category of Web3 applications. A suite of blockchain application development efforts is recreating lending, borrowing, trading, and yield generation without a bank or brokerage acting as an intermediary.

Where the numbers stand in 2026

DeFi has had a turbulent year. According to data aggregator DeFiLlama, cited by CryptoRank, total value locked (TVL) across DeFi fell in every month of 2026, dropping roughly 39% from about $115 billion in January to around $70 billion by late June.

The decline reflects three forces: a broader crypto market correction (Bitcoin fell more than 50% from its October 2025 all‑time high), compressed yields that pulled speculative capital out of leveraged strategies, and a costly wave of exploits. CryptoRank recorded 121 hacks totaling roughly $942 million in losses through the first half of the year, with the April breaches of Drift Protocol ($295 million) and KelpDAO ($293 million) accounting for more than half of that total. The KelpDAO incident alone triggered a 46% drop in Aave's TVL as attackers used stolen collateral to borrow against the protocol.

That said, industry researchers note that this contraction is far milder than the 2021 to 2022 crash, when TVL fell by more than 70% in seven months. And beneath the headline number, DeFi's composition is shifting toward durability: CoinLaw reports that real‑world asset (RWA) TVL reached $26.01 billion in mid‑2026, the only major DeFi category showing sustained institutional inflow. Meanwhile, stablecoin circulating supply climbed to $314 billion, roughly 4.4 times the size of total DeFi TVL, underscoring that stablecoins are becoming a payments rail in their own right rather than just DeFi collateral.

Leading platforms

Aave, Uniswap, and Morpho Blue continue to anchor the lending and trading side of DeFi, with the top five lending protocols now holding roughly 75% of all DeFi lending TVL, a sign of capital consolidating around better‑audited, higher‑revenue platforms rather than spreading across the long tail.

Why does it still matter?

Even after this year's drawdown, DeFi offers 24/7 markets, transparent on‑chain settlement, and access to yield and credit for users outside the traditional banking system. For businesses evaluating Web3 software development, 2026's lesson is that sustainable protocol revenue and third‑party security audits now matter more than headline APYs.

2. NFTs and Real‑World Asset (RWA) Tokenization

The NFT market has completed what one industry analysis calls a "brutal but productive transformation." The speculative profile‑picture era has largely ended; monthly Ethereum NFT trading volume has stabilized around $720 million, still 79% below its 2022 peak of $3.5 billion, and the median NFT has lost roughly 79% of its value since 2022. But the technology underneath NFTs (verifiable, transferable ownership) has found much sturdier ground in real‑world asset tokenization.

The RWA breakout

On‑chain tokenized real‑world assets grew roughly fourfold between 2025 and 2026, surpassing $26 billion, according to CleanSky's analysis of the sector, with figures from RWA.xyz showing a similar trajectory, reaching $24 billion by February 2026, up 266% during 2025. Tokenized U.S. Treasuries make up the largest slice of that figure at roughly $9.6 billion, boosted heavily by BlackRock's BUIDL fund, which alone holds about $1.7 billion in assets. Real estate tokenization is following close behind, with the market for tokenized property projected to reach $78 billion by the end of 2026.

What's driving the shift

Tokenization lets investors buy fractional stakes in previously illiquid assets (a slice of a commercial property, a share of a private credit fund, a portion of a fine‑art piece) and trade those stakes with far more liquidity than the underlying asset would normally allow. NFT‑based digital identity is emerging alongside this trend, functioning as a secure, user‑controlled credential that can be verified by third parties without exposing the underlying personal data.

Enterprise use cases

Corporations are now using NFTs for supply‑chain provenance, employee credentialing, brand loyalty programs, and intellectual property management as practical infrastructure rather than collectible art. Fashion houses are tying digital collectibles to physical product releases, sports leagues are linking NFTs to ticketing and experiential perks, and music labels are experimenting with fractional rights ownership.

3. Blockchain Gaming and Play‑to‑Earn Ecosystems

Blockchain gaming, often bundled with the term "GameFi," has matured past the early play‑to‑earn hype cycle into a more sustainable model centered on actual gameplay quality. Market estimates vary widely depending on methodology, but most converge on a market in the $28 to $48 billion range for 2026, with longer‑term forecasts stretching into the hundreds of billions by the early 2030s as the sector scales alongside mainstream gaming.

Adoption data

SQ Magazine's 2026 review of crypto gaming statistics reports that daily unique active wallets in blockchain gaming average 4.8 million, that blockchain games retain 35% of players monthly (with 52% still active after 90 days), and that 76% of blockchain gamers cite true asset ownership (the ability to actually own, sell, or trade in‑game items) as the primary draw. Mobile is increasingly the primary access point, with industry researchers estimating that roughly half of Web3 gaming activity now happens on smartphones.

Studios to watch

Sky Mavis (Axie Infinity, Ronin Network), Animoca Brands (The Sandbox, Mocaverse, and a portfolio of more than 400 companies), Immutable, and Mythical Games remain the dominant infrastructure players. Notably, Sky Mavis retired the original Axie Infinity Classic in mid‑2026 to concentrate resources on its successor, Axie Infinity Origin, and halted token emissions specifically to curb bot farming, a sign that studios are now actively engineering against the exploitative economics that defined the first play‑to‑earn wave.

The retention challenge

Not every metric points up. Web3 gaming token valuations fell an estimated 69% year‑over‑year in 2025, and venture funding into the sector slowed sharply, a reminder that, as with DeFi, capital is now rewarding games with real players and durable economies over token‑emission‑driven growth.

4. Decentralized Autonomous Organizations (DAOs)

DAOs remain Web3's answer to organizational governance: blockchain‑coordinated groups where token holders vote on treasury allocation, protocol upgrades, and strategic direction instead of relying on a traditional corporate hierarchy. MakerDAO (now largely operating as Sky), Uniswap, and Compound continue to be cited as the clearest examples of governance token holders directly steering multi‑billion‑dollar protocols.

In 2026, DAO structures are increasingly embedded inside other Web3 application categories rather than standing alone. Market research on Web3 gaming, for instance, finds that 38% of new blockchain games now incorporate DAO‑style governance, letting player communities vote on updates, economic parameters, and treasury spending. That trend mirrors what's happening across DeFi and NFT communities more broadly: DAOs are becoming a governance layer built into applications, rather than a category unto itself.

The tradeoffs businesses are weighing

DAOs offer transparency and distributed decision‑making, but they also introduce coordination costs, legal ambiguity around liability, and voter‑turnout problems common to any large, loosely organized group. Enterprises exploring DAO‑based governance in 2026 are generally pairing it with legal wrapper structures (foundations or LLCs) to resolve jurisdictional and liability questions that pure on‑chain governance doesn't answer on its own.

5. Enterprise and Institutional Web3: Supply Chain, Identity, and Payments

The fifth major application category isn't consumer‑facing at all. It's the quiet, high‑volume adoption of Web3 software development inside large enterprises, spanning supply‑chain provenance tracking, decentralized identity systems, and blockchain‑based settlement infrastructure.

Institutional settlement is scaling fast. JPMorgan's Onyx platform has expanded from internal transfers to offering tokenized settlement services directly to clients, and Coinbase reported $2.03 billion in institutional revenue in a single quarter of 2025, an indication of how much compliant crypto infrastructure large financial institutions are now routing through. Government bodies are participating too. California's DMV, for example, has digitized tens of millions of vehicle title records onto blockchain‑based infrastructure to reduce fraud and paperwork friction.

Regional dynamics

North America still leads Web3 market share (39.05% in 2025, per Mordor Intelligence), but Asia‑Pacific is the fastest‑growing region, projected to expand at roughly 45.9% CAGR through 2031, driven by Singapore's licensing regime, Japan's tax incentives and national Web3 roadmap (which helped prompt Sony's $3.5 million stake in Startale Labs), and the sheer scale of crypto adoption in India and Indonesia, which rank first and third globally by adoption volume. Europe's MiCA framework, meanwhile, is pushing identity- and privacy‑focused Web3 applications that align with GDPR's emphasis on user data control.

What enterprises are actually building

The most common builds are supply‑chain provenance tools that let a retailer verify a product's origin at every step, decentralized identity credentials that reduce reliance on centralized password databases, and tokenized loyalty or credentialing systems that give customers portable, verifiable proof of purchase or certification.

Industry Impact: Where Web3 Is Landing Hardest

- Finance: DeFi protocols and tokenized RWAs are compressing settlement times and expanding access to yield‑bearing instruments once reserved for institutional investors.

- Gaming and entertainment: Studios are rebuilding play‑to‑earn economics around retention and genuine gameplay rather than token emissions.

- Retail and luxury goods: Brands are using NFTs for authentication, limited releases, and loyalty programs tied to real purchases.

- Real estate: Fractional tokenized ownership is opening property investment to smaller‑ticket investors, with the tokenized real estate market on pace to hit $78 billion by year‑end.

- Government and identity: Public agencies are piloting blockchain‑based records to cut fraud and processing time.

Future Trends to Watch Through the Rest of 2026

- RWA tokenization keeps outpacing native crypto assets. With institutional players like BlackRock and Fidelity now running production‑scale tokenized funds, this is likely to remain the fastest‑growing corner of Web3 through year‑end.

- Regulatory clarity becomes a competitive advantage. The Clarity Act's progress through Congress, alongside MiCA and DAC8 in Europe, is pushing serious capital toward compliant platforms and away from unregulated venues.

- Security consolidation. After a record‑setting second quarter for DeFi exploits, expect continued consolidation of capital toward audited, higher‑revenue protocols rather than emissions‑driven newcomers.

- AI and Web3 convergence. Dynamic NFTs, AI‑assisted smart contract auditing, and AI‑driven personalization inside dApps are becoming standard rather than novel.

- Cross‑chain interoperability. Expect continued investment in bridges and universal wallet standards that let assets and identity move between Ethereum, Solana, and Layer‑2 networks without friction.

FAQs

1. What are Web3 applications?

Web3 applications, or dApps, are software programs that run on blockchain networks using smart contracts instead of centralized servers, giving users direct ownership and control over their data, assets, and digital identity.

2. Is DeFi still a good example of Web3 in 2026?

DeFi remains one of the largest Web3 categories by capital deployed, though 2026 has brought a notable TVL contraction driven by market conditions and security incidents. Analysts generally view the sector as consolidating around more secure, revenue‑generating protocols rather than disappearing.

3. Are NFTs still relevant?

Speculative NFT trading has cooled significantly since 2022, but the underlying technology has shifted toward real‑world asset tokenization, digital identity, and enterprise use cases. These are the areas with far more institutional backing than the original collectibles boom.

4. How much does Web3 app development cost?

Costs vary widely based on blockchain choice, smart contract complexity, security auditing requirements, and whether the project needs custom infrastructure (like a dedicated Layer‑2 chain) versus building on existing rails. Businesses typically work with a Web3 development company to scope requirements before committing to a specific architecture.

5. What's the difference between Web3 development and traditional software development?

Web3 development centers on smart contracts, decentralized storage, and blockchain integration rather than centralized databases and servers, and it requires additional emphasis on security auditing, since smart contract code is often immutable once deployed.

Conclusion

Web3 applications in 2026 look meaningfully different from the speculative wave of 2021. DeFi is smaller but more disciplined; NFTs have shed most of their speculative volume in favor of real‑world asset tokenization and enterprise utility; blockchain gaming is optimizing for retention over emissions; DAOs are becoming an embedded governance layer rather than a standalone trend, and institutions are running production‑scale settlement and tokenization infrastructure rather than pilots. For businesses evaluating decentralized applications, blockchain application development, or a broader Web3 development strategy, the throughline for 2026 is clear: durable revenue, regulatory compliance, and real user demand now matter more than raw growth metrics, and the applications built on those foundations are the ones actually revolutionizing their industries.

CTA: Thinking about where Web3 fits your business? Mazilytic builds custom software, including blockchain and Web3 applications, scoped around real use cases and real compliance requirements. Get in touch.